All Categories

Featured

Table of Contents

:max_bytes(150000):strip_icc()/do-beneficiaries-pay-taxes-life-insurance.asp-final-7e81561536514dbdb30500ba1918afb3.png)

Area 691(c)( 1) offers that a person that includes an amount of IRD in gross earnings under 691(a) is enabled as a reduction, for the very same taxable year, a part of the estate tax obligation paid by reason of the addition of that IRD in the decedent's gross estate. Typically, the amount of the reduction is calculated utilizing estate tax values, and is the quantity that births the same proportion to the estate tax obligation attributable to the net worth of all IRD things included in the decedent's gross estate as the value of the IRD consisted of in that person's gross income for that taxed year bears to the value of all IRD items consisted of in the decedent's gross estate.

Section 1014(c) gives that 1014 does not put on residential property that constitutes a right to get an item of IRD under 691. Rev. Rul. 79-335, 1979-2 C.B. 292, addresses a circumstance in which the owner-annuitant purchases a deferred variable annuity agreement that gives that if the owner passes away before the annuity beginning day, the named beneficiary may choose to get the here and now built up value of the agreement either in the kind of an annuity or a lump-sum repayment.

Rul. 79-335 concludes that, for objectives of 1014, the contract is an annuity explained in 72 (as then essentially), and as a result gets no basis change because the proprietor's fatality because it is regulated by the annuity exemption of 1014(b)( 9 )(A). If the beneficiary chooses a lump-sum settlement, the unwanted of the amount got over the quantity of consideration paid by the decedent is includable in the beneficiary's gross earnings.

Rul (Fixed annuities). 79-335 concludes that the annuity exception in 1014(b)( 9 )(A) puts on the agreement explained in that ruling, it does not especially attend to whether amounts gotten by a recipient under a deferred annuity agreement in excess of the owner-annuitant's financial investment in the agreement would go through 691 and 1014(c). Had the owner-annuitant surrendered the contract and got the amounts in extra of the owner-annuitant's financial investment in the agreement, those amounts would certainly have been revenue to the owner-annuitant under 72(e).

How is an inherited Flexible Premium Annuities taxed

In the existing instance, had A surrendered the agreement and obtained the amounts at problem, those amounts would certainly have been income to A under 72(e) to the extent they went beyond A's financial investment in the agreement. Accordingly, amounts that B gets that exceed A's financial investment in the contract are IRD under 691(a).

Rul. 79-335, those quantities are includible in B's gross earnings and B does not receive a basis change in the agreement. B will certainly be qualified to a reduction under 691(c) if estate tax obligation was due by factor of A's fatality. The result would coincide whether B obtains the fatality advantage in a swelling amount or as routine settlements.

COMPOSING INFORMATION The primary writer of this income ruling is Bradford R.

Do you pay taxes on inherited Annuity Beneficiary

Q. How are just how taxed as strained inheritance? Is there a difference if I acquire it straight or if it goes to a trust for which I'm the beneficiary? This is a great inquiry, yet it's the kind you should take to an estate preparation lawyer that understands the details of your situation.

What is the relationship between the departed proprietor of the annuity and you, the beneficiary? What kind of annuity is this?

We'll think the annuity is a non-qualified annuity, which indicates it's not component of an Individual retirement account or other competent retired life strategy. Botwinick claimed this annuity would certainly be included to the taxed estate for New Jersey and government estate tax obligation functions at its date of death worth.

Fixed Income Annuities inheritance tax rules

person spouse exceeds $2 million. This is called the exemption.Any amount passing to an U.S. resident spouse will certainly be completely excluded from New Jersey inheritance tax, and if the proprietor of the annuity lives to the end of 2017, after that there will be no New Jacket inheritance tax on any type of amount due to the fact that the inheritance tax is arranged for abolition starting on Jan. There are government estate tax obligations.

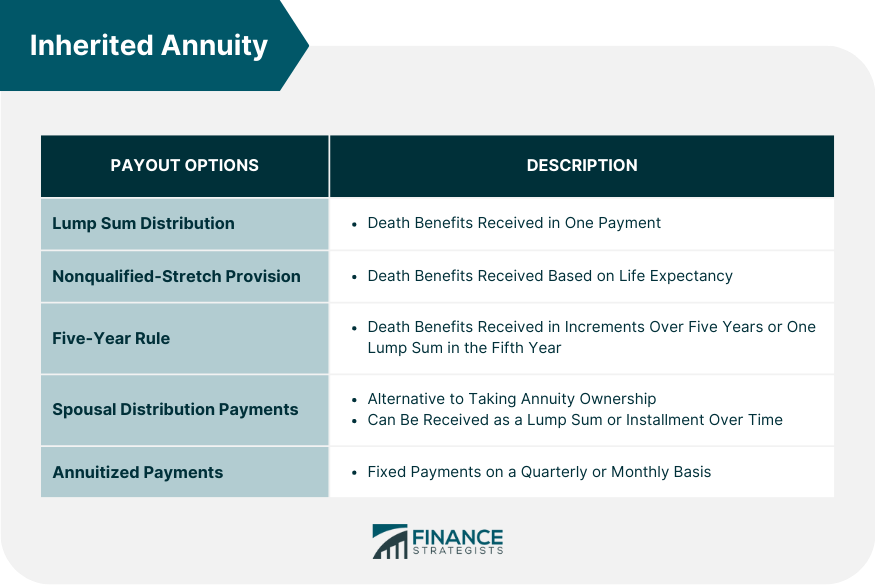

"Currently, revenue taxes.Again, we're thinking this annuity is a non-qualified annuity. If estate taxes are paid as an outcome of the inclusion of the annuity in the taxable estate, the recipient might be qualified to a reduction for inherited earnings in respect of a decedent, he stated. Beneficiaries have several choices to take into consideration when picking exactly how to get money from an inherited annuity.

{kind=link}

Table of Contents

Latest Posts

Decoding Fixed Income Annuity Vs Variable Annuity Everything You Need to Know About Financial Strategies Defining the Right Financial Strategy Pros and Cons of Various Financial Options Why Fixed Vs V

Highlighting Fixed Annuity Vs Equity-linked Variable Annuity A Closer Look at What Is A Variable Annuity Vs A Fixed Annuity What Is the Best Retirement Option? Advantages and Disadvantages of Deferred

Highlighting Fixed Vs Variable Annuities A Closer Look at How Retirement Planning Works What Is the Best Retirement Option? Benefits of Choosing the Right Financial Plan Why Choosing the Right Financi

More

Latest Posts